Home Insurance Discounts for Impact Windows in Pensacola: 2026 Savings Guide

- ECWA

- May 15

- 12 min read

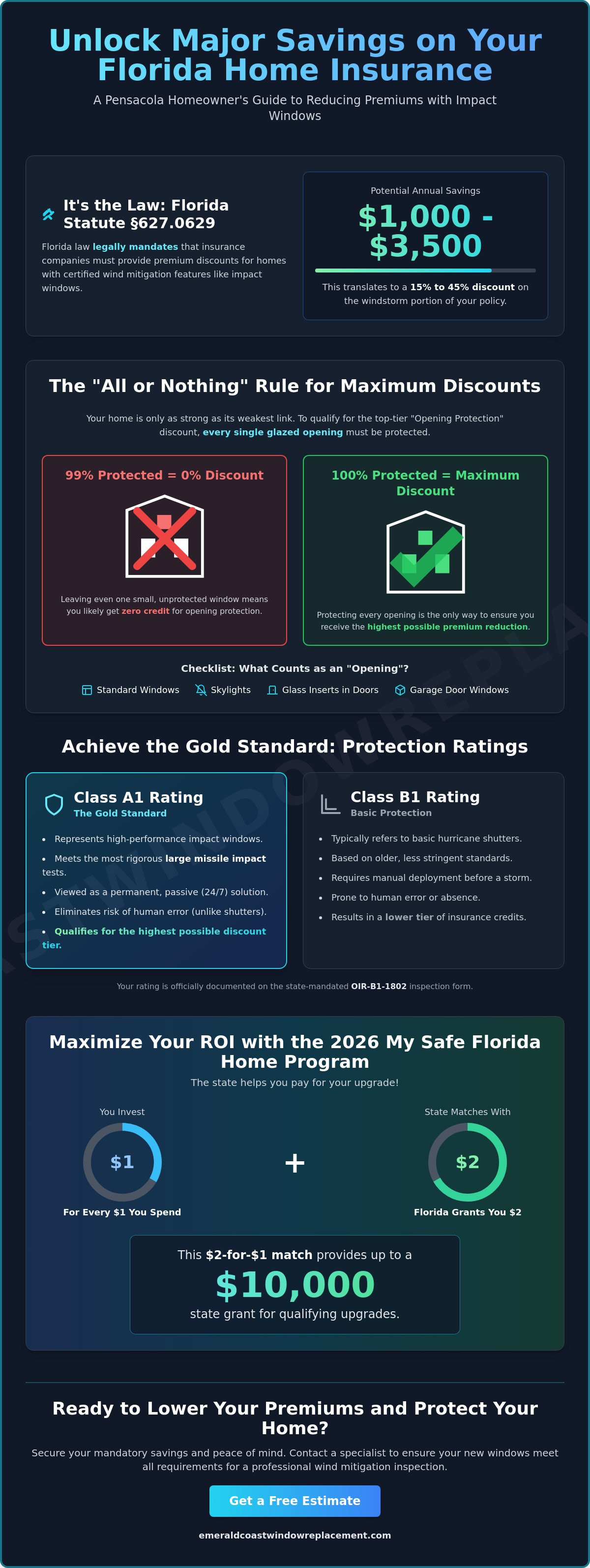

Did you know that Florida Statute §627.0629 legally mandates that your insurance company must lower your premiums if you protect your home against wind damage? You've likely watched your annual statements climb higher every year, leaving you feeling frustrated and priced out of your own neighborhood. It's a common struggle across the Panhandle as we face increasingly unpredictable seasons. Securing home insurance discounts for impact windows Pensacola isn't just about safety. It's a critical financial strategy to reclaim control over your household budget.

You'll learn exactly how to manage the 2026 wind mitigation requirements to unlock credits that can save you between $1,000 and $3,500 annually on your coastal policy. We'll break down the updated OIR-B1-1802 inspection form that became mandatory on April 1, 2026. We'll also explain the current status of My Safe Florida Home grants and provide a clear roadmap to securing your mandatory savings. From high-performance vinyl windows to elegant casement styles, upgrading your home is the most effective way to lower your bills while ensuring your family's peace of mind.

Key Takeaways

Understand how Florida Statute 627.0629 legally mandates insurance carriers to provide premium credits for certified opening protection.

Discover how to maximize home insurance discounts for impact windows Pensacola by meeting the specific wind-borne debris zone codes for Escambia County.

Learn why the "all or nothing" rule requires every glazed opening to be protected before you can qualify for the maximum wind mitigation credit.

Explore the 2026 My Safe Florida Home grant structure, where the state provides a $2-for-$1 match up to $10,000 for qualifying residential upgrades.

Identify the essential documentation your window specialist must provide to ensure your high-performance windows pass a professional wind mitigation inspection.

Table of Contents

How Impact Windows Trigger Insurance Savings in Florida

Florida law doesn't leave your insurance savings to chance. Under Florida Statute 627.0629, every residential insurance provider in the state must offer premium credits for homes that have verified wind-loss mitigation features. This isn't a "maybe" or an optional perk; it's a legal requirement designed to encourage homeowners to harden their properties against the Gulf Coast’s volatile weather. When you search for home insurance discounts for impact windows Pensacola, you're really looking at a strategy to reduce your home’s "opening protection" risk profile. By upgrading to high-performance windows, you're signaling to your insurer that your property is a low-risk asset, which forces them to lower your rates.

Insurance companies categorize your home’s vulnerability based on how well your windows, doors, and other entry points can withstand flying debris. Impact-resistant windows are viewed as a superior, permanent solution compared to traditional hurricane shutters. While shutters require a human to be present and physically deploy them before a storm, hurricane windows provide passive protection 24 hours a day. Insurers trust this "always-on" resilience more, as it eliminates the risk of human error or absence during a sudden weather event. This reliability often leads to more favorable underwriting and a smoother path to those mandatory credits.

The 'All or Nothing' Rule for Opening Protection

One common mistake homeowners make is thinking that protecting most of their windows is enough. In the eyes of an insurance company, your home is only as strong as its weakest link. To qualify for the maximum "Opening Protection" discount, every single glazed opening must be impact-rated. This includes your standard windows, but it also covers skylights, glass inserts in front doors, and even the small windows in your garage doors. If you protect 95% of your home but leave one small bathroom window vulnerable, you'll likely receive zero credit for opening protection on your policy. It's a binary system; you either have a fully protected envelope or you don't.

Class A1 vs. Class B1 Ratings

When a professional performs a wind mitigation inspection, they use the state-mandated OIR-B1-1802 form to document your home's defenses. The form uses specific codes to rank your protection level based on testing standards. A "Class A1" rating is the gold standard, indicating that every opening meets the most rigorous testing standards for large missile impact. "Class B1" typically refers to basic shutter systems or older, less stringent standards. Achieving a Class A1 rating with high-performance impact windows ensures you're eligible for the highest possible tier of premium reduction available in Escambia County.

Calculating Your Potential Discounts: What Pensacola Homeowners Save

Homeowners in Escambia County often face some of the highest insurance premiums in the state. Because we live in a high-velocity hurricane zone, the windstorm portion of your policy makes up a massive chunk of your annual bill. By installing certified impact-resistant products, you can expect home insurance discounts for impact windows Pensacola ranging from 15% to 45% on that windstorm portion. Unlike a one-time tax credit or a grant, these savings are recurring. They stay on your policy year after year, effectively paying for the windows over time through lower overhead.

Beyond the base premium, these upgrades also lower your 'loss of use' coverage costs. Insurers recognize that impact-resistant glass significantly reduces the likelihood that a storm will make your home uninhabitable. Since the risk of you needing a hotel for six months is lower, the cost to insure against that possibility drops too. This multi-layered reduction in your risk profile makes high-performance windows one of the smartest financial moves a coastal homeowner can make. In many cases, coastal Florida residents see annual insurance savings between $1,000 and $3,500 after verifying their upgrades.

Regional Premium Factors in the Florida Panhandle

Your specific address in the Panhandle dictates the scale of your return on investment. If you're living in a newer build in inland Milton, your baseline premiums are already relatively low. However, for a beachfront property on Pensacola Beach or a historic home in North Hill, the dollar-value of a 45% discount is substantial. The age of your home also plays a role. Older structures that haven't been "hardened" face steep surcharges that disappear once you verify full opening protection. When you compare these savings against the window replacement cost in Gulf Breeze or surrounding areas, the break-even point often arrives much sooner than expected. Many local residents also utilize the My Safe Florida Home Program to offset the initial investment, making the transition to a safer home even more affordable.

Secondary Financial Benefits Beyond Insurance

While the insurance check is the main draw, the hidden savings are equally impressive. High-performance windows feature advanced Low-E coatings that block solar heat gain, which is a necessity during our sweltering July and August months. This leads to a noticeable drop in monthly energy bills. Additionally, the Pensacola real estate market places a high premium on storm-ready homes. Buyers are often willing to pay more for a house that already has verified protection, knowing they won't have to deal with the stress of immediate upgrades. Most importantly, you gain the peace of mind that your family is safe from June 1 through November 30. If you're considering an upgrade, exploring a variety of sliding windows or double-hung windows can help you find the perfect balance of style and resilience.

The Wind Mitigation Inspection: Your Key to Unlocking Credits

Securing your savings requires more than just a receipt from a window company. To activate home insurance discounts for impact windows Pensacola, you must undergo a formal wind mitigation inspection. This process provides the objective data your insurance carrier needs to recalculate your risk profile. In the Pensacola area, a standalone inspection typically costs between $75 and $135 as of May 2026. It's a small price to pay for a report that can save you thousands over the life of your policy.

The process follows a specific sequence to ensure accuracy. First, ensure every window and door is fully installed and functional. Next, hire a licensed Florida home inspector or engineer. Since April 1, 2026, inspectors must use the updated OIR-B1-1802 (Rev. 04/26) form. This version is more detailed than previous iterations, requiring precise documentation of your home's defenses. Once the report is in your hands, submit it to your insurance agent immediately. Don't wait for your renewal period; many carriers will apply Florida wind mitigation credits mid-term and issue a pro-rated refund. Finally, verify that the credit appears on your next policy declaration page to confirm the discount is active.

What the Inspector Looks for in Impact Windows

An inspector doesn't just glance at the glass; they look for specific engineering markers. They search for the permanent etching in the corner of the glass, which lists the manufacturer and the impact rating. They also record the Florida Product Approval or Miami-Dade Notice of Acceptance (NOA) numbers. These codes prove the windows were tested against high-velocity debris. Beyond the glass, they examine the frames and how they're anchored into your home's structure, ensuring the entire unit works as a single, resilient barrier.

Preparation Checklist for Pensacola Residents

To make the inspection as smooth as possible, have your documentation ready. Keep your manufacturer spec sheets and municipal permits in a single folder. The inspector needs to see that the job was done to code. Clear any furniture or window treatments that might block access to the frames. Before you book, visit the Florida Department of Business and Professional Regulation (DBPR) website to verify the inspector’s license is active and in good standing. This extra step ensures your report is valid and won't be rejected by your insurance company.

Maximizing ROI with the My Safe Florida Home Program in 2026

As of May 2026, the My Safe Florida Home (MSFH) program remains the most powerful financial tool for Pensacola residents looking to harden their homes. The 2025-2026 funding cycle was backed by a substantial $352 million allocation. While lawmakers have already agreed on an additional $100 million for the 2026-2027 budget, acting now is vital while current funds are still accessible. This program offers a matching grant structure that is incredibly favorable for the homeowner. The state contributes $2 for every $1 you spend, up to a maximum grant of $10,000. For a project totaling $15,000, your out-of-pocket cost is only $5,000. This low entry point makes securing home insurance discounts for impact windows Pensacola a reality for many who previously felt priced out of the market.

Eligibility is primarily tied to your primary residence and requires a valid homestead exemption. The program currently prioritizes seniors aged 60 and older and low-income homeowners, ensuring that those most vulnerable to rising costs receive help first. A major benefit of the MSFH process is the initial wind inspection provided by the state at no cost. This professional assessment identifies exactly which upgrades will yield the highest protection. It also creates a clear paper trail that simplifies the process of claiming your mandatory insurance credits once the project is finished. By the time your high-performance windows are in place, you'll have the verified documentation your insurer needs to lower your rates.

2026 Grant Application Strategy

To navigate the MSFH portal for the fastest approval, ensure you have your property tax records and proof of homestead ready before you begin the digital application. The program requires homeowners to work with MSFH-approved contractors in the Panhandle to maintain grant eligibility. These vetted professionals understand the specific engineering requirements of our coastal region. You should apply as early as possible in the fiscal year when funding is replenished to ensure your application is processed before the seasonal surge in interest.

Combining Grants with Insurance Credits

The true value of this program is seen when you calculate the long-term "Net Cost." Homeowners who complete improvements through MSFH and report them to their carriers save an average of over $900 per year on their premiums. When you combine a $10,000 grant with five years of these recurring insurance savings, the initial investment is often entirely recovered. Choosing energy-efficient windows further boosts your ROI by slashing monthly cooling costs. Since the federal tax credit for windows expired at the end of 2025, this state grant is the most significant incentive left for Florida residents. To find the right fit for your home’s aesthetic and safety needs, you can browse a variety of casement windows or picture windows that meet the program's strict impact standards.

Finding Vetted Impact Window Specialists in Pensacola

Your investment in safety only works if the installation is as resilient as the glass itself. In Escambia County, the Wind-Borne Debris Zone (WBDZ) regulations are incredibly specific. If an installer fails to meet these structural requirements, your wind mitigation inspector will have no choice but to fail the report. This oversight could completely void your eligibility for home insurance discounts for impact windows Pensacola. Working with an unlicensed or inexperienced crew isn't just a safety risk; it's a financial liability that can cost you thousands in lost premium credits. Permits matter. Local expertise ensures that every anchor and seal meets the rigorous demands of our coastal climate.

Vetting a contractor requires more than a quick glance at a website. You need to verify their local Pensacola references and ensure they carry active liability and workers' compensation insurance. A truly professional team will be happy to provide their Florida license number and documentation for the high-performance windows they intend to use. They should be intimately familiar with local permitting processes and the documentation required for the OIR-B1-1802 form we discussed earlier. When you choose a specialist who understands the nuances of the Florida Panhandle, you ensure your home remains a safe, high-value asset for years to come.

Why a Neutral Advisor Matters

Many homeowners feel overwhelmed by the high-pressure sales tactics common in the window industry. Emerald Coast Window Authority acts as your local protector and neutral guide. We help you skip the scripted sales pitch and move straight to the technical specs of vinyl windows or sliding windows that actually fit your home's needs. By providing a consultative approach, we ensure you have the information necessary to compare multiple estimates without the stress of a "buy now" ultimatum. Our goal is to connect you with licensed, local Panhandle specialists who value craftsmanship over quick transactions. This transparency allows you to make an informed decision based on durability and aesthetic value rather than a salesman's quota.

Take the Next Step for Your Pensacola Home

The path to a more secure and affordable home is straightforward. By selecting the right hurricane-impact windows and following up with a professional inspection, you unlock recurring home insurance discounts for impact windows Pensacola that protect your household budget. Whether you prefer the classic look of double-hung windows or the expansive views of picture windows, the financial and safety benefits are undeniable. Don't let another hurricane season pass with rising premiums and an unprotected home. Use our free tool to begin your journey toward verified resilience and long-term savings.

Secure Your Savings and Protect Your Pensacola Home

Protecting your home from the Gulf's unpredictable weather shouldn't be a financial burden. By leveraging Florida's mandatory premium credits and the current 2026 My Safe Florida Home grant cycle, you can transform your property into a resilient fortress while significantly lowering your overhead. Remember that full "Opening Protection" is a binary requirement. Ensuring every window and glass door meets the highest impact standards is the only way to guarantee the maximum credit on your policy. This methodical approach ensures that your investment pays for itself through recurring annual savings.

When you're ready to explore home insurance discounts for impact windows Pensacola, don't settle for high-pressure sales pitches or vague promises. Our team acts as a neutral advisor to help you navigate the technical specs of high-performance windows. We connect you with vetted, licensed Panhandle specialists who know Escambia County building codes inside and out. We take pride in helping our neighbors skip the stress of traditional sales and get straight to the facts of structural resilience. Take control of your home’s safety and your insurance bills today.

You've worked hard to build a life on the coast. Let's make sure it's protected with the quality and transparency you deserve.

Frequently Asked Questions

Will my insurance company pay for the impact windows?

No, your insurance provider won't pay the upfront cost for the windows or their installation. Instead, Florida law requires them to provide recurring home insurance discounts for impact windows Pensacola once the project is finished. These credits reduce your annual premium, allowing you to recover your investment over time through significantly lower insurance bills.

How much does a wind mitigation inspection cost in Pensacola?

In the Pensacola and Florida Panhandle area, a standalone wind mitigation inspection typically costs between $75 and $135 as of May 2026. This fee is paid to a licensed inspector who verifies your home's protective features. It's a small but necessary investment to provide the documentation your insurance company needs to apply your mandatory credits.

Do I need to replace every window to get the insurance discount?

Yes, you must protect every glazed opening to qualify for the full "Opening Protection" discount. This includes all windows, glass doors, and skylights. If you leave even one small window unprotected, insurers will generally deny the credit because the home’s structural envelope remains vulnerable to pressure changes during a hurricane.

How long does the wind mitigation credit last on my policy?

Most insurance carriers in Florida honor a wind mitigation report for five years. After this period, you'll likely need to hire an inspector to submit a fresh report to maintain your home insurance discounts for impact windows Pensacola. Some companies may request an update sooner if you make other major structural changes to the property.

Can I get a discount for hurricane shutters instead of impact windows?

You can get a discount for shutters, but impact windows are often preferred by insurance companies because they provide permanent, passive protection. Shutters only work if they're properly deployed before a storm hits. Insurers value the "always-on" nature of high-performance windows, which eliminates the risk of human error or the homeowner being away during an event.

What is the OIR-B1-1802 form, and do I need to fill it out?

The OIR-B1-1802 is the Uniform Mitigation Verification Inspection Form required by the state of Florida. You don't fill this out yourself. A licensed home inspector or engineer must complete it after examining your home. The newest version of this form, Rev. 04/26, became mandatory for all new inspections starting April 1, 2026.

Are there local Pensacola grants available for window replacement in 2026?

Yes, the My Safe Florida Home program still has grant money available as of May 2026. The program offers a matching grant where the state pays $2 for every $1 you spend, up to $10,000. Current funding cycles are prioritizing low-income homeowners and seniors aged 60 and older to help them harden their homes against storms.

Does the age of my roof affect the window discount?

The age of your roof is a separate category on the wind mitigation report and won't change the specific credit you get for your windows. However, wind mitigation discounts are cumulative. A newer roof combined with full opening protection will result in the highest possible overall premium reduction and better long-term insurability for your coastal home.

Comments